Unlocking Profitability: A Comprehensive Guide to Variable Costing Method

In the dynamic world of business, understanding your costs is paramount to making informed decisions and achieving sustainable profitability. One powerful tool in the cost management arsenal is the variable costing method. This approach offers a distinct perspective compared to traditional absorption costing, focusing on the behavior of costs rather than their function. This article will delve into the intricacies of the variable costing method, exploring its principles, advantages, disadvantages, and practical applications.

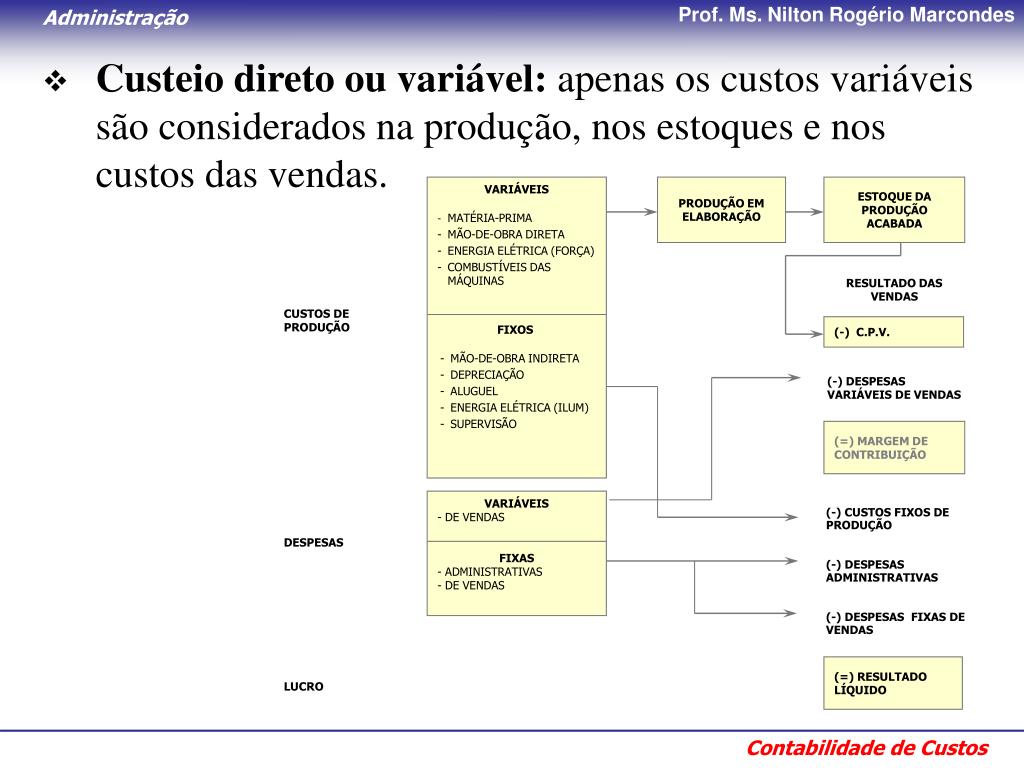

What is Variable Costing?

The variable costing method, also known as direct costing, is an accounting approach that only includes variable manufacturing costs in the cost of a product. These variable costs typically encompass direct materials, direct labor, and variable manufacturing overhead. Fixed manufacturing overhead, on the other hand, is treated as a period cost and is expensed in the period it is incurred, regardless of the number of units produced. This contrasts sharply with absorption costing, where fixed manufacturing overhead is allocated to each unit produced.

Understanding the difference is crucial. With variable costing, the cost of a product reflects only the costs that change with the level of production. This provides a clearer picture of the incremental cost of producing each additional unit. [See also: Absorption Costing vs. Variable Costing]

Key Components of Variable Costing

To fully grasp the variable costing method, it’s essential to understand its key components:

- Direct Materials: The raw materials that are directly used in the production of a product.

- Direct Labor: The wages paid to workers who are directly involved in the production process.

- Variable Manufacturing Overhead: The indirect manufacturing costs that vary with the level of production, such as electricity, supplies, and machine maintenance.

- Fixed Manufacturing Overhead: The indirect manufacturing costs that remain constant regardless of the level of production, such as rent, depreciation, and insurance. Under variable costing, these are treated as period costs.

Advantages of Variable Costing

The variable costing method offers several advantages that make it a valuable tool for managerial decision-making:

- Improved Decision-Making: By focusing on variable costs, managers can more easily determine the profitability of individual products or services. This allows for better pricing decisions, product mix optimization, and make-or-buy decisions. Understanding the true incremental cost of production is vital for effective decision-making.

- Better Cost Control: Variable costing highlights the impact of changes in production volume on profitability. This encourages managers to focus on controlling variable costs and improving efficiency.

- Simpler to Understand: The variable costing method is generally easier to understand than absorption costing, as it avoids the complexities of allocating fixed manufacturing overhead. This simplicity can lead to better communication and understanding across different departments within the organization.

- More Accurate Performance Measurement: Because fixed costs are treated as period costs, the variable costing method provides a more accurate picture of the profitability of a particular period. This can be particularly useful for evaluating the performance of managers and departments.

- Facilitates CVP Analysis: Variable costing is essential for cost-volume-profit (CVP) analysis, which helps businesses understand the relationship between costs, volume, and profit. CVP analysis can be used to determine break-even points, target profit levels, and the impact of changes in sales volume on profitability.

Disadvantages of Variable Costing

While the variable costing method offers numerous benefits, it also has some limitations:

- Not GAAP Compliant: The variable costing method is not generally accepted accounting principles (GAAP) compliant for external reporting purposes. Companies must use absorption costing for financial statements that are presented to investors and creditors.

- Potential for Misinterpretation: If not properly understood, the variable costing method can lead to misinterpretations of profitability. For example, a company that produces a large number of units but sells few may show a higher profit under variable costing than under absorption costing, even though the company is actually incurring significant costs to store unsold inventory.

- Difficult to Apply in Some Industries: The variable costing method can be difficult to apply in industries with high fixed costs and low variable costs. In these industries, the allocation of fixed costs may be more important for determining the true cost of a product.

- Inventory Valuation Issues: Since fixed manufacturing overhead is not included in inventory cost under variable costing, the value of inventory may be understated. This can affect financial ratios and other performance metrics.

Variable Costing vs. Absorption Costing

The primary difference between variable costing and absorption costing lies in the treatment of fixed manufacturing overhead. Under variable costing, fixed manufacturing overhead is treated as a period cost and is expensed in the period it is incurred. Under absorption costing, fixed manufacturing overhead is allocated to each unit produced and is included in the cost of inventory. This difference can have a significant impact on a company’s reported profits, especially in periods of fluctuating production levels.

When production exceeds sales, absorption costing will generally result in higher reported profits than variable costing. This is because a portion of the fixed manufacturing overhead is deferred to future periods as part of the inventory cost. Conversely, when sales exceed production, variable costing will generally result in higher reported profits than absorption costing. This is because the fixed manufacturing overhead is expensed in the current period, regardless of the level of production.

Calculating Profit Under Variable Costing

To calculate profit under the variable costing method, you will need to follow these steps:

- Calculate the contribution margin: This is the difference between sales revenue and variable costs.

- Subtract fixed costs from the contribution margin: This will give you the net operating income.

Example:

Let’s say a company sells 1,000 units of a product for $100 each. The variable cost per unit is $60, and the fixed costs are $20,000.

Sales Revenue: 1,000 units x $100 = $100,000

Variable Costs: 1,000 units x $60 = $60,000

Contribution Margin: $100,000 – $60,000 = $40,000

Net Operating Income: $40,000 – $20,000 = $20,000

Therefore, the net operating income under the variable costing method is $20,000.

Practical Applications of Variable Costing

The variable costing method can be applied in a variety of business settings to improve decision-making and cost control. Some common applications include:

- Pricing Decisions: Variable costing can help businesses determine the minimum price they can charge for a product or service while still covering their variable costs.

- Product Mix Decisions: Variable costing can help businesses determine which products or services are the most profitable and should be emphasized.

- Make-or-Buy Decisions: Variable costing can help businesses decide whether to manufacture a product internally or outsource it to an external supplier.

- Performance Evaluation: Variable costing can be used to evaluate the performance of managers and departments by focusing on their control over variable costs.

- Budgeting and Forecasting: Variable costing can be used to develop more accurate budgets and forecasts by separating fixed and variable costs.

Conclusion

The variable costing method is a valuable tool for understanding and managing costs. While it is not GAAP compliant for external reporting, it offers several advantages for internal decision-making, including improved profitability analysis, better cost control, and simpler understanding. By focusing on the behavior of costs, the variable costing method provides a clearer picture of the incremental cost of production and helps managers make more informed decisions. Businesses should carefully consider the advantages and disadvantages of variable costing before implementing it. [See also: Cost Accounting Methods]